2023

simplification

standard costs

Under the CAP 2023-2027, the support of the variety of types of interventions, (art.83 of EU Reg. 2021/2115), may take the form of unit costs, among the others. This is the option that the Managing Authority of the CAP strategic plan of Hungary took on board for the implementation of training actions for farmers.

According to applicable regulation, the amounts for the unit costs shall be established in one of the following ways:

(a) a fair, equitable, and verifiable calculation method based on:

(i) statistical data, other objective information, or an expert judgment, (ii) verified historical data of beneficiaries; or

(iii) the application of usual cost accounting practices of beneficiaries.

(b) draft budgets established on a case-by-case basis and agreed on ex-ante by the body selecting the operation in the case of interventions in the wine and apiculture sectors or the body approving the operational programs referred to in Article 50 in the case of interventions in the other eligible sectors;

(c) in accordance with the rules for the application of corresponding unit costs, lump sums, and flat rates applicable in Union policies for a similar type of intervention;

(d) in accordance with the rules for the application of corresponding unit costs, lump sums, and flat rates applied under support schemes funded entirely by the Member State for a similar type of intervention.

Accordingly, the Managing Authority had the necessity to determine the unit cost of reference for training interventions.

The solution adopted refers to the verified historical data of the beneficiaries (option a) ii)) collected for the Agri-food and preparatory training interventions that were funded under the Rural Development Programme 2014-2020.

In view to determine reliable unit costs, the identified solution applied a four-step approach:

1. Identification of the different types of training courses and the respective costs

On the basis of the experience of the previous financial period, the unit costs of four different types of training have been determined for the period 2023-2027, as their cost structure (e.g. depending on the length of the training material, the ratio of practical and theoretical hours, the number of organizational cost items) varies considerably. The following types of training are considered separately, taking into account both the current legal and regulatory environment and the expected needs of the final beneficiaries (e.g. farmers):

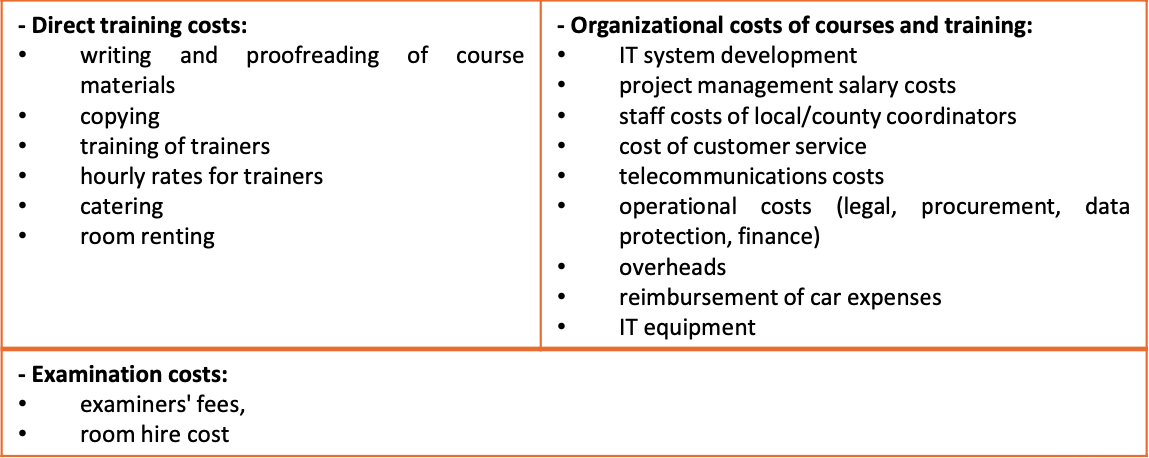

2. Definition of eligible costs

The costs cover mainly staff costs (including coordination, instructors, and examiners), but also the preparation of didactical materials and the renting of rooms.

Overall, the following types of costs have been considered in determining the unit cost:

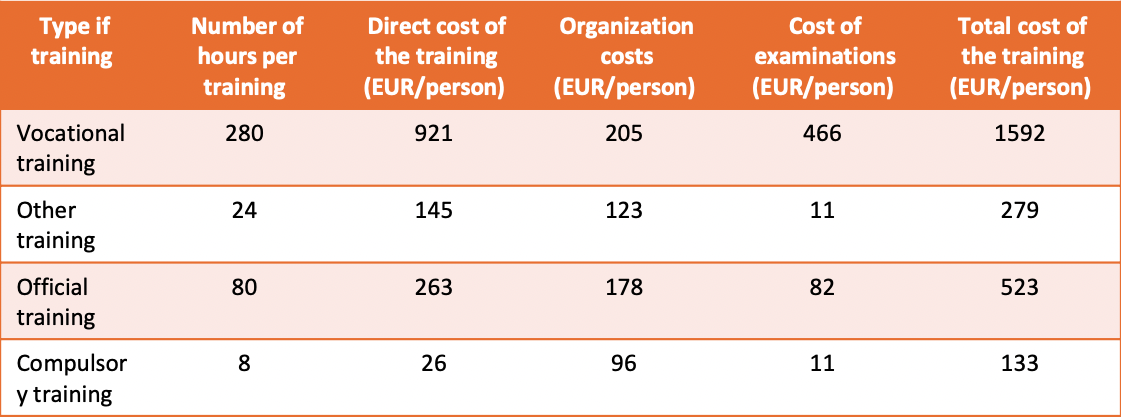

3. Determination of costs per capita for each type of training course

For each type of training, the training organizations supported by the Rural Development Programme 2014-2020 have determined the average hourly rates, specific organization and examination fees, and cost items used in their practice, which have been sum-up1. For examination fees, current market (or statutory) fees were considered. Based on the data collected, the per capita costs of the types of training supported are as follows:

Table 1 Cost per capita of subsidized training

Note: Data are based on reports of training bodies supported by the Hungarian RDP 2014-2020

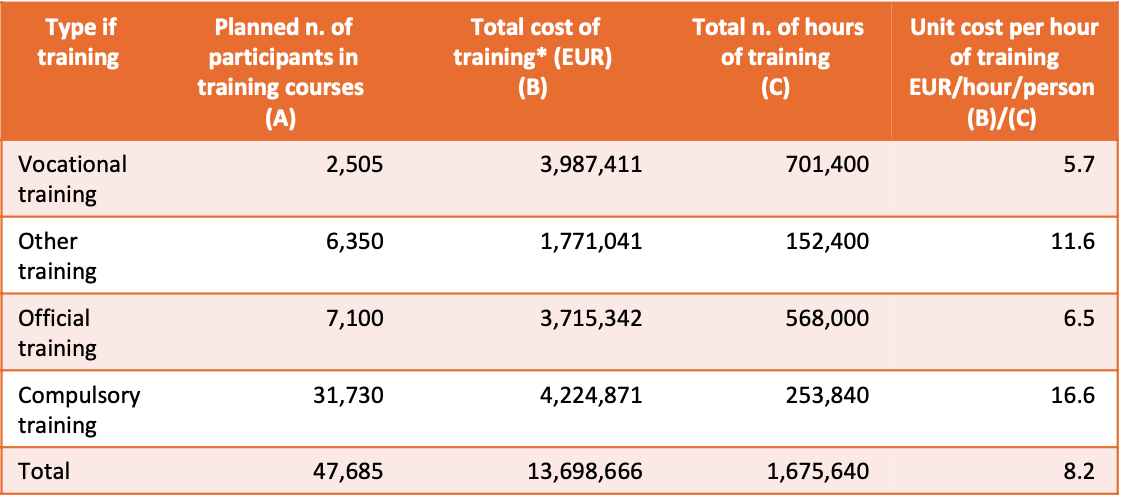

4. Calculation of the unit costs per hour by type of training

For each type of training, the unit costs per hour are based on the number of participants planned in previous years, the total number of hours, and the total cost per person of the training

Table 2 Estimated unit costs per hour by type of training

*Total training cost per person x number of participants planned.

Note: The exchange rate used is HUF 365/EUR

The calculations thus show that the overall average unit cost of the subsidized training is therefore EUR 8.2/hour.